Original Link: https://www.anandtech.com/show/3665/apples-intrinsity-acquisition-winners-and-losers

Apple's Intrinsity Acquisition: Winners and Losers

by Ganesh T S on April 28, 2010 6:30 PM EST- Posted in

- Intrinsity

- Samsung

- Hummingbird

- Gadgets

- Smartphones

- Mobile

A Brief History of Intrinsity

Apple made its third semiconductor company acquisition in a stealthy manner by not making any public announcements. The alert online community discovered via some careful sleuthing that Austin, TX based Intrinsity Inc's employees had started to work for Apple from the beginning of April 2010. SEC filings made by Apple for its quarterly earnings report on April 20, 2010 indicated that Apple spent around $325 million for business acquisitions. Though Intrinsity's name wasn't publicly disclosed, a knowledge of Apple's recent acquisitions indicated that the total amount was spent on Quattro Wireless, LaLa and Intrinsity. Quattro Wireless was purchased for $275 million and TechCrunch had previously suggested that LaLa was purchased for $17 million. Based on this, some infer that Apple spent less than $50 million in order to grab Intrinsity's tech and employees. However, the NYTimes report confirming Apple's acquisition quoted analyst Tom Halfhill in suggesting a purchase price of $121 million. The analyst contends that that Apple may not have paid all the money at once or 100% in cash. That, he says, may account for the lower estimates that people derive from Apple's publicly disclosed expenditures. This is very much within the realms of possibility, but people suggesting that Apple paid less than $50 million for Intrinsity say that this doesn't take into account the financial state of Intrinsity in the few months preceding the acquisition. Let us take a brief detour to trace Intrinsity's history and analyze this further.

Technology

Founded in 1997 by 22 veterans in the microprocessor design industry, the firm initially worked towards developing interesting circuit design techniques and related design infrastructure for performance improvement (speed of circuit operation) using domino logic. If you are interested in the details, there are some course slides from MIT to help you out. Intrinsity's website also had a 'Technology' section devoted to detailing their version of domino logic. The summary is that it is a circuit level technique which gets rid of the slow components inside the transistor level implementations of the various logic gates / functions. This makes it unsuitable for the usual design flow (writing RTL code in a hardware description language, followed by synthesizing it using automated computer tools to get a gate level description, which is then translated to the actual chip layout by placing and routing the standard cells corresponding to the generated gate netlist). Creating standard cells for domino logic is not an easy task, and companies often prefer to just handcraft the relevant logic in domino style in the slowest part of the circuit. Intrinsity has developed a design flow using domino logic cells, called Fast14. However, the whole flow is specific to a particular foundry's process node, and shifting to a new foundry or process requires quite a bit of rework. Usually, the foundries provide the standard cells, but, in this case, one is reliant on Intrinsity to supply the cells. This is usually much later than the delivery date for the static CMOS standard cells. This is the main reason for the flow to be not as popular with fabless semiconductor companies as the usual design flow. On the other hand, companies like Intel devote huge amount of resources to perfect the layout of each and every gate in their pipeline to get the requisite performance. It is believed that Intel also uses a variant of domino logic for designing many components in their datapath. Intrinsity's approach (as well as the associated delay in taping out the chip) lies somewhere between the static CMOS standard cells flow used by most companies and the full custom approach used by ones with lots of resources.

Business

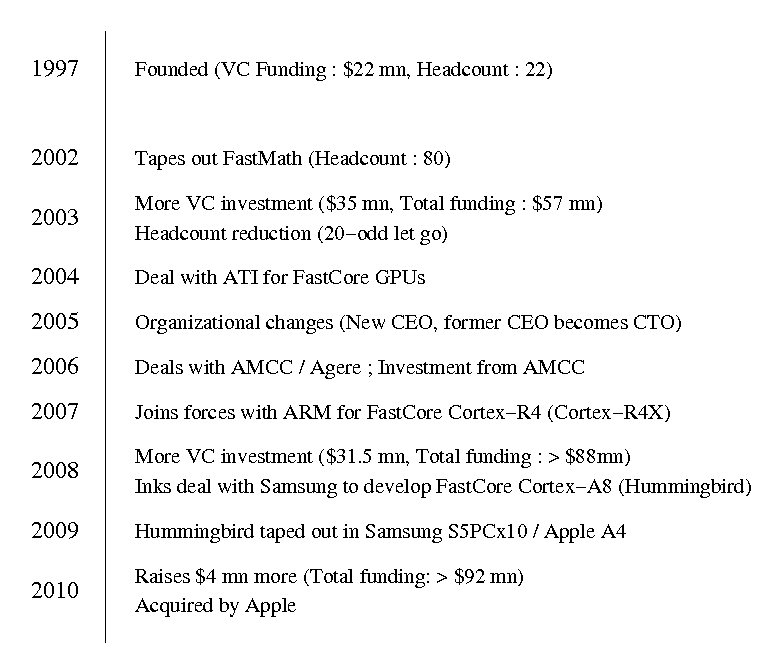

After five years of flying under the radar (by which time the headcount had increased to 80-odd and $15 million had been burned through), Intrinsity finally managed to tape out a chip using their domino logic scheme towards the end of 2002. This DSP-centric processor (called the FastMath) was able to clock an impressive 2GHz in TSMC's 130nm process. It enjoyed critical acclaim, but business for this chip wasn't exactly forthcoming. In May 2003, with just around $7 million left in the bank, Intrinsity was forced to get back to the VCs for more funding. An investment of $35 million followed which was supposed to be used for sales efforts. However, taking the processor into full production had to be shelved following general market apathy towards a DSP from a relatively unknown company. In order to keep down the cash burn rate, 20-odd employees had to be let off. With no revenue stream available, Intrinsity decided to begin efforts to license their technology to other fabless semiconductor companies.

Intrinsity Inc's Business Timeline

As outlined in the 'Technology' section, convincing companies to ditch their original design flow for something novel like domino logic is not easy. In February 2004, they entered into a deal with ATI, wherein, the technology would be used for a multitude of future ATI GPU designs. This lent them financial stability for some years. In early 2005, there were some organizational changes, with the old CEO moving into the role of a CTO, and the hiring of a new CEO. Deals with AMCC and Agere Systems followed in 2006, generating some more revenue. For AMCC, Intrinsity helped develop the Titan core based on the embedded PowerPC architecture. AMCC even invested and got some stake in the company. Business began to look up as ARM joined hands with Intrinsity to develop a FastCore version (the tag given by Intrinsity to any logic core synthesized with their Fast14 domino technology) of the Cortex-R4 called as the Cortex-R4X in 2007. Analysts expected a FastCore version of the Cortex-A8 to have very good performance too, but ARM didn't appear too interested in pursuing that line. Despite all these deals, the expenses were still high, and Intrinsity had to snag more investments. In early 2008, $31.5 million was obtained in a Series E funding round, bringing the total money raised to more than $88 million (The amount of money invested by AMCC in exchange for stake in the company isn't public).

In September 2008, Samsung went against ARM's suggestion that any semi-custom implementation of the Cortex-A8 wouldn't be faster than TI's OMAP3 version. They inked a deal with Intrinsity to develop a FastCore version of the Cortex-A8 called as the Hummingbird. In the meanwhile, Apple was also looking for a way to speed up the Cortex-A8 for their iPad. It is believed in industry circles that Samsung asked Intrinsity develop a FastCore version of the Cortex-A8 at the behest of Apple for A4, and also ended up using it for the S5PC110 / S5PV210 after splitting the cost (according to rumors). The hardening was completed in July 2009, just in time for the rest of the A4 SoC to be taped out for the iPad and the S5PC110 for the Samsung Galaxy S.

Intrinsity also raised $4 million in late January 2010 from 11 different investors, bringing the total amount raised by the company closer to the $100 million mark. The LinkedIn page for Intrinsity suggests that they had around 120 people at the time of acquisition. For such a company, $4 million is barely sufficient for a quarter's expenses. It must have been known at that point of time that the company was fast running out of cash and would need to be sold. The above timeline also indicates that Intrinsity had to keep hunting for investment and was never able to sustain profits for long. The LinkedIn page of one of Intrinsity's employees indicates 'Controller at Intrinsity (Assets Acquired by Apple Computer)' in the 'Past Experience' section. It is believed that 'asset acquisition' is different from a straightforward 'acquisition' in the sense that it is more of a 'fire sale' rather than a purchase based on the true valuation of the company's technology. This is not surprising, considering the fact that Intrinsity's financial position appears to have been precarious in January 2010. All these tend to make some people in the industry believe that Apple could have got hold of the company by offering them a rock-bottom price. This, they suggest, may also be the reason why Intrinsity wouldn't want the purchase price made public, as it would show their investors as well as the value of their technology in poor light.

While introducing the iPad in January 2010, Steve Jobs specifically commented on A4 as the best and most complicated chip Apple had ever designed. Industry watchers were skeptical when it became obvious that the A4 was just a SoC hooking up various IPs available from different companies. Once it became evident that Apple had indeed purchased Intrinsity, Steve Jobs's claim began to make more sense. In effect, Apple had developed their most advanced silicon to date!

Apple and Intrinsity's Perspective

Historically, Apple has not had much luck with their semiconductor company acquisitions. In November 1999, they acquired Raycer Graphics for $15 million dollars, supposedly for the 3D graphics related patents that the company held. People continued to speculate for 2 or 3 years after this wondering when the products from this acquisition would replace Nvidia's role in Apple computers. Unfortunately, this never came to pass, and people from the Raycer acquisition just moved on to join companies like SGI and Nvidia. In April 2008, PA Semi was acquired for $278 million. Their claim to fame was a 64 bit dual core processor called the PWRficient. The analysts were greatly surprised at this acquisition since PA Semi's IP had no place in the roadmap of any of Apple's products (except, probably, the Apple TV) since its power consumption was too high at 25W. The consensus was that the purchase was made for the manpower with VLSI experience that PA Semi would provide to Apple's team for designing chips for future generation of products in the iPhone / iPod / iPad line. Then, again, most of the PA Semi engineers have since moved on from Apple to work in a startup named Agnilux (which was recently acquired by Google), and Apple has been forced to supplement the workforce with reputed chip engineers from other companies.

When seen in the above context, it is really easy to determine why Apple needed to acquire Intrinsity. Being the force behind the performance of the Cortex-A8 in the A4, it makes sense for them to acquire the engineering talent and the technology behind this. Not only would it improve the performance of the ARM cores in the future members of the A4 family (Intrinsity was supposedly working on hardening the FastCore version of Cortex-A9), it would also prevent the competition (read, Samsung) from utilizing this technology to make fast app processors for phones such as the Samsung Galaxy S. As noted in the previous paragraph, Apple has never been able to retain the important employees from its semiconductor acquisitions. It remains to be seen how much of a leeway from the usual Apple work culture is given to Intrinsity after the acquisition, as this would probably decide how much of the talent actually continues to remain in Apple to contribute down the road.

From Intrinsity's perspective, the acquisition probably comes as a relief. As can be seen from the Intrinsity timeline on the previous page, the company has been reliant on a few big customers for revenue and had to get back to the venture capitalists for more and more funding every few years. A successful semiconductor company startup usually manages to become cash-flow positive after 4-5 years, and eschews further VC investment to prevent stock dilution unless their revenue stream fails to match up with their plans. Once a company goes past four or so rounds of funding, there is an increased pressure from the VCs to generate returns on their investment. There are two exit choices: one is to get acquired by a bigger company for the technology and patents, and the second is to go for an IPO. With Apple showing interest in the technology, and IPO not really looking like an option due to the lack of a sustained profit curve, there was only one way to go for Intrinsity. Now, with more than $100 million dollars invested, was it really a good exit for Intrinsity's investors? If MPR's sources (which Tom Halfhill stands by with conviction) are correct, at $121 million, the investors just about managed to get their cash back. Unfortunately, $20 - $30 million over 13 years is really not such a great return, particularly when the investment amounts are adjusted for inflation. On the other hand, if Apple managed to dictate terms, a purported purchase price of less than $50 mn would imply that the investors' money just went down the drain. However, the asset acquisition at least ensured that the current employees had their jobs saved by shifting to Apple. From Apple's perspective, $121 million or sub-$50 million really doesn't matter, since the amounts happen to be a drop in the bucket for a company with more than $40 billion in the bank.

From a technology perspective, domino logic has long been regarded with suspicion by many people because of the associated problems. Though speed and performance increase, the power consumption as well as integration with the rest of the design flow remains an issue. Fast14 technology doesn't advocate usage of the domino logic in all parts of the chip, but only in the critical path (slowest sequence of gates in the circuit which pulls down the operating frequency for the whole chip). This is done in order to minimize die area and power consumption penalties. As process geometries shrink, some engineers feel that leakage, noise and clock skew related issues become more and more difficult to surmount. Further, NDL technology (the traditional name given to Fast14) results in increased number of interconnects. Unfortunately, interconnects don't scale as well as transistors do when process geometries shrink. More time needs to be spent in fine tuning the layout to achieve timing closure and handling interconnect loads. So, it is quite possible that despite the automated methodology that Intrinsity possesses, getting a FastCore version of the Cortex-A9 in, say, the 32nm node, may take much more time, than, say, in the 45nm node.

Unlike the traditional processor market where Intel and AMD can take 2 years or more and use a lot of manpower to churn out a processor at a particular node, players in the application processor market often rely on being the first company to take advantage of a particular node. If the Intrinsity group's schedules slip, Apple might find itself in the back foot against competitors like Nvidia and TI with the Tegra and OMAP series respectively. Note that the A4 with Intrinsity's Cortex-A8 is actually up against Nvidia's Tegra 2 which already has the Cortex-A9 at the same 1 GHz (admittedly in TSMC's 40nm node). Samsung is expected to move towards the 32nm node around the same time that TSMC gets ready to implement 28nm, which Nvidia would presumably use. There is also the small matter of the difference in the manpower behind the Nvidia's Tegra group in charge of hardening the ARM processor and Intrinsity's. Then, again, Apple always has better software and marketing to paper over the cracks in the application processor. In that case, however, Intrinsity's purchase wouldn't have given them any more advantage than what they already possess.

Apple has long claimed that they needed to design their own CPU in the iPad series to decide where the exact performance push would go. With Intrinsity, they were able to get a fast core and split the hardening cost with Samsung. It is not exactly clear how Apple can customize the CPU any further than what Intrinsity would do as an outside job without holding an architecture license from ARM (MPR suggests that Apple also possesses an architecture license, though we are unable to confirm this from other sources). If Apple does go through the architecture license route, they are looking at a 4 year investment cycle (similar to what Qualcomm spent on the Scorpion core in Snapdragon). It is also not clear whether Intrinsity's knowhow includes architecture level manipulation of the Cortex implementations. It is definitely clear that the current Cortex FastCore versions didn't have any micro-architectural modifications, and was a cycle-accurate representation of ARM's original microarchitecture.

If Apple was hoping to cut down on the cost of hardening future CPU cores by purchasing Intrinsity, it doesn't seem like such a great decision keeping the above points in mind. On the other hand, if the aim was to prevent the competition from getting access to this technology, it may succeed to quite an extent. All in all, it can't be said that Apple's acquisition of Intrinsity is a slam dunk.

The Rest of the Industry

What repercussions does this acquisition have for the rest of industry? It is still not clear whether Intrinsity would continue to support any of their existing customers (AMD/ATI and AMCC -- whether they are still using FastCore technology is not known). However, we can safely say that the FastCore version of the Cortex-A8 on Samsung's 45nm node is the final Intrinsity product available for other fabless semiconductor companies to license. This hardened macro (called as the Hummingbird) has found a place in some of Samsung's app processors, but we are not aware of any other licensees for this.

Of all the companies involved, it appears that Samsung's app processor division would suffer the most in this transaction. It is quite possible that they were counting on a FastCore version of the Cortex-A9 at the 32nm node for their next generation product in the S5PC line. The online rumour mill suggests that Intrinsity had already been working on a FastCore version of Cortex-A9, but it is not clear whether it was Samsung who had requested it (most likely). The status of this FastCore after Apple's acquisition remains unclear.

While Samsung's app processor division could end up unhappy, things continue to bode well for Samsung's foundry business. Apple was never likely to move away from them for future members of the A4 product line, but Intrinsity's acquisition and their previous experience with Samsung's process flow only continue to strengthen this belief.

Intrinsity's technology, back in 2001, was probably a bit ahead of its time. Undoubtedly, their most outstanding success to date seems to be the Hummingbird core in the 45nm node, showing how their technology has matured and delivered outstanding results for a company of Apple's stature to use in their own products. Unfortunately, for the rest of the industry, the technology has been rendered no longer licensable. With the relevant patents now belonging to Apple, it is unlikely that other companies can benefit from Fast14 technology of any form in their own product lines. The pity is that these may be product lines such as the embedded PowerPC market for control and telecom applications (this is where AMCC's Titan core designed with help from Intrinsity's FastCore technology is used) where Apple has no presence. Hopefully, the industry would continue to innovate and get past the loss of this promising technology.

Final Words

In closing, it can be said that there are no outright winners in the asset acquisition. While Intrinsity's investors may have just about broken even or may have even had to get out with a big loss, Apple has its hands full in trying to get some returns for the investment in their third semiconductor company acquisition. In particular, considering the fact that they don't seem to have had much success with the first two, it will be interesting to watch how Apple's management style works in a small fabless semiconductor company. The nature of Intrinsity's technology also doesn't seem very amenable to the fastest-time-to-market nature of the application processor market, and this only makes Apple's task that much more difficult. Current licensees of Intrinsity's technology and the Samsung application processor group (particularly if the rumors of Intrinsity's current activities with respect to the Cortex-A9 turn out to be true) seem to be left in limbo. The industry, in general, has lost the ability to take advantage of a technology whose time seemed to have just arrived.

Note: We are grateful to Tom Halfhill for his invaluable inputs to this story. If you require a professional analysis of the acquisition, please check out his piece "Why Apple Wants Intrinsity" in the April 26th, 2010 issue of Microprocessor Report.